Dividend for 2019/20

Another reminder to you all that there is now tax on dividend! This has been the case since 6 April 2016. The tax-free dividend allowance is £2,000 from the 2018/19 tax year and beyond.

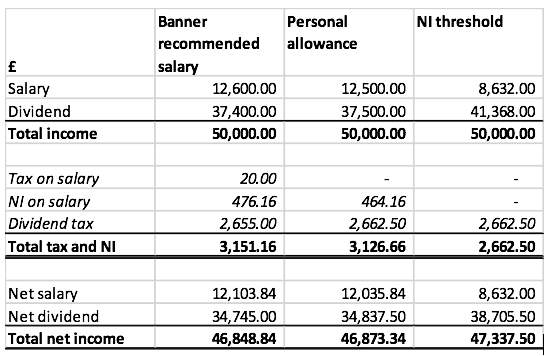

What I have done is gone through some examples below of how much dividend you can take while remaining in the basic rate threshold of 7.5% tax on the dividend. The below assumes no other income besides salary and dividend.

Remember dividend is the last income item to be taxed, therefore, if you have property rental income or foreign income then you would have to reduce your dividend by the total of the other income in order to remain in the basic rate threshold.

Remember you should yourselves be aware of how much dividend you are taking out of the business (see point 3 below). We have a dividend tax calculator on our website which you can use to work out your tax.

You can take more than the basic rate threshold in dividend and the below table is just given as guidance.

I have listed out below some useful hints and tips.

- As a basic rule move 20% of your revenue into a separate business savings account and use this to pay your corporation tax. The remaining 80% is available for you to take out in a combination of reimbursed petty cash expenses, salary and dividend.

- You must maintain enough money in the company account to pay your corporation tax. Cash and accounts work on two separate principles. Cash works on an actuals basis. Accounts work on an accruals basis meaning that at your year-end there will be liabilities which are outstanding (the biggest of which is corporation tax) and the Company must hold enough money to pay these liabilities. If it doesn’t then effectively you have taken the ‘would be corporation tax’ money out as a Directors Loan.

- Take out dividend separately to salary and reimbursed expenses. You should do separate transfers for salary, dividend and reimbursed expenses using the correct reference for each. DO NOT take lumpsums to account for all three; salary, dividend and reimbursed expenses.

- If your tax liability through self-assessment is greater than £1k then HMRC will ask you to pay next year’s tax in advance via two payments on account, one due on 31 January and the other due on 31 July.